From "Transitory" to "Panic"?

This week has been all about the implosion of the global economy from the perspective of the hegemon. “It’s the economy, stupid”.

With many central bankers scrambling to tame inflation added with shambolic fiscal policies.

This week is one for the history books.

But we begin from yesterday as many waited with bated breath for Fed chairman, Jerome Powell’s announcement of the concluded FOMC meeting.

*TLDR (courtesy, Bloomberg):

The Fed raised its benchmark rate by 75 basis points -- the biggest increase since 1994 -- to a range of 1.5%-1.75%, in line with investors’ and economists’ expectations

Kansas City Fed President Esther George dissented in favor of a 50 basis-point hike

FOMC adds a line saying it’s “strongly committed to returning inflation to its 2% objective” and removes prior language that said the FOMC “expects inflation to return to its 2% objective and the labor market to remain strong”

Reiterates path on balance-sheet reduction that took effect June 1, shrinking bond portfolio by $47.5 billion a month and stepping up to $95 billion in September

The Fed sharply raised its rates outlook (to meet market expectations) and sharply lowered its growth and employment outlooks.

With recession already baked in, we anticipate more further rate increases although the rate of change is more important in my opinion. Maybe, a soft landing is on the horizon? Well, the Fed says by 2024 but according to Frances Donald, global head of macro strategy at Manulife Asset Management:

“The crux of today is that the Fed is catching up to market thoughts: front-loaded hiking leading to a rise in unemployment, followed by cuts in 2024. The Fed is happy to hike into weakness -- which risks recession -- and will subsequently cut rates. The Fed’s outlook is gentler and smoother than what is likely to happen as the 0.4 increase in the unemployment rate is likely too complacent about the risks to the other side of the Fed’s mandate. We expect the easing cycle to be needed and enacted in 2023, not 2024.”

This hike will only crush demand and fuel an increase in unemployment levels.

Lesson here: You simply can’t kill demand and expect growth!

So as we transition to era of high inflation rates, expect lower purchasing power which means lower sales. In turn, lower sales means less revenue for companies to hire/expand, as most will cut cost. Labor Cost is critical to business.

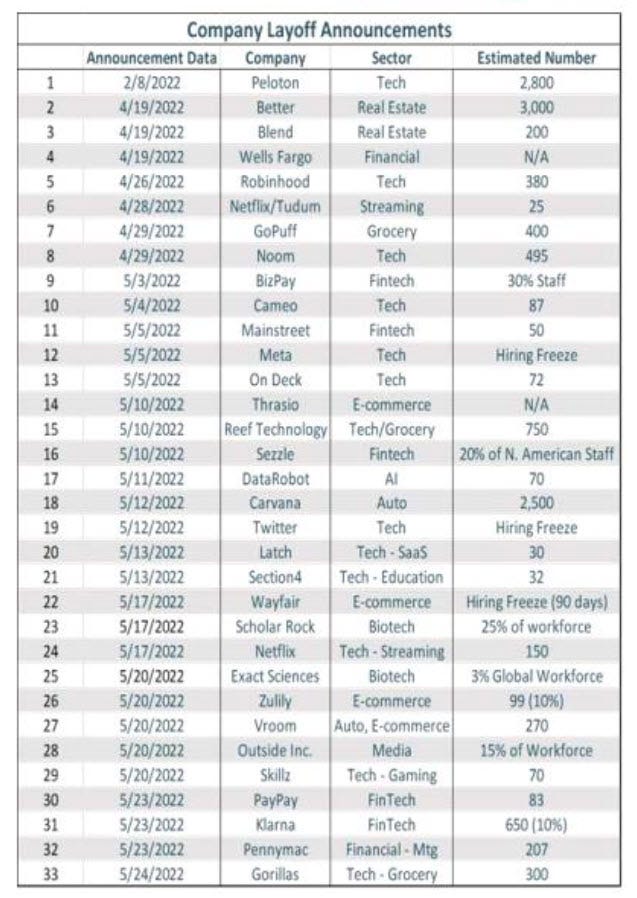

Spoke too soon as there is already a wave in tech layoffs:

And counting,

Crypto space is not immune to the whiplash:

No one is immune, as we all drink from the same punch bowl cocktail. Even emerging markets (EM).

Concluding with Rabobank’s global strategist Michael Every:

“There is real EM schadenfreude in current Western struggles. In 1997, and long before that in Latin America, EM crises were treated thus: raise rates; cut state spending; force recession; sell off state assets (to the West); and sell off private-sector assets at fire-sale prices (to the West). Yet when the West faced its own crisis in 2008, what did it do? Cut rates; do QE; and bail everyone guilty out. If the Fed now has to keep hiking in 75bps steps and can’t cut rates and do more QE without inflationary consequences, then West perhaps faces a 2008 redux without a safety net.

..Of course, you can’t eat schadenfreude, served hot or cold (or crypto). DM may hate the surge in commodity prices, the dollar, and Eurodollar rates, but for many EM it is an outright calamity.

If the Fed keeps tightening, we face global pain, most so in EM. If the Fed backs off “because markets”, we face global inflation. Either way today, après Fed, the deluge.”

More pain to come either way. Make sure not to panic!

See you tomorrow!

- Ope